What Habits Hurt Your Financial Goals

For the last 10 years I’ve spent pretty much every single day working in a bubble the revolves around finance & making money. After finishing my economics degree at university in 2010 I started to work for a large accountancy firm, and after qualifying there as a chartered accountant, I began my career in investment banking, which I’m now in my 7th year of doing.

From this experience of being constantly surrounded by bright money motivated people whilst learning all about the workings of the finance world, I’ve developed a solid understanding of all of the bad money habits that people develop that makes them poorer than they should be. Whilst some of my friends might claim that this understanding and avoidance of bad spending habits makes me tight – I disagree, in fact, I think spotting and avoiding these bad money habits is something that allows you to stay in control of your personal finance and puts you on a path towards wealth and financial freedom.

So today, I’m going to be sharing with you the most common bad money habits that I see, habits that you should avoid if you want ensure that you never feel like you’re chained to a desk and forced to work for the rest of your life.

1. Not Actively Saving

The first bad money habit I see, is where people don’t choose to actively set aside and save a proportion of their wages. Instead, they get their pay packet at the end of each month, they pay their rent and their bills, and then they use the rest to eat out, go shopping, go clubbing, and so on, and then by the third or fourth week of the month when they think “oh I should probably start saving”, they see what’s left over in their account and realise there’s not much if anything at all.

And because saving money is so far down on many people’s priority lists, this behaviour happens month in month out, and results in people living pay-check to pay-check, not saving a penny and not putting themselves any closer to being able to eventually escape the rat race.

So, if this sounds like you – to give yourself a fighting chance of one day getting to be financially free, instead of just hoping that you’ll have some money left over at the end of each month after you’ve lived your life, put together a monthly budget that maps out all of your expenses and includes an savings target of ideally 20% of your income.

And the best way to hit that savings target, is to think of it like a bill that has to be paid first at the same time as your rent. Once you adopt the mindset that saving a proportion of your income is non-negotiable, and you then map out your monthly budget with all of your income and other expenses, you’ll quickly realise that you’re probably spending way more than you thought you were on things like meals out, clubbing, shopping and so on.

Now I’m not saying to kill every element of fun that you have with a a bid to save more money each month, but what I am saying is: give yourself a solid understanding of your spending habits by making a budget, and then adjust those non-essential spending habits slightly so that you’re able to consistently hit your monthly savings goal.

Taking a proactive approach to financial decisions like that is going to be way more effective at helping you to build long term wealth, instead of just waiting to see what’s left over in your bank account at the end of each month, which is an activity that’s only going to keep you poor.

2. Avoiding Lifestyle Creep

If you work for a fairly big company or in an industry that has a lot of progression opportunities, then at some point you’re probably going to become a victim of ‘lifestyle creep’. Lifestyle creep happens when an increase in a person’s income leads to a permanent increase in their spending on living costs and nonessential expenses. In other words, things that once used to be luxuries and treats when you first started working, are now perceived to be necessities that you absolutely can’t be doing without. And without thinking about it, these necessities aren’t always going to be obvious expenses such as a requirement to fly business class or stay in 5 star hotels. Instead, examples could be only ever buying designer gear, or buying 3 or 4 coffees and eating out for lunch whilst you’re at work every day.

Becoming an unknowing victim of lifestyle creep means 1 thing – that you’re spending more on non-essential items than you need to be, which is ultimately going to harm your financial health you’re your financial security. So to stop this becoming a bad money habit that spirals out of control, whenever you get a pay rise or your living circumstances change, update any spending or budgeting process that you have according to the 50/30/20 – 50% of your income goes on needs, 30% on wants, and 20% on your savings accounts.

3. Bad Debt

These days, with the rise of online shopping and the movement away from cash, owning a credit card is pretty much a standard procedure. Now, credit cards can be great tools to have in order to build your credit score and to benefit from things such as cashback and cheap business class flights. But unfortunately, due to their high spending allowances and ease of use, many people develop the bad money habit of consistently buying what they cant afford and wracking up lots of bad expensive debt as a result.

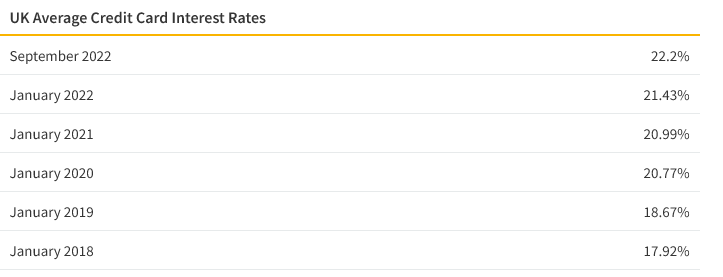

Credit card debt has an average interest rate of 22%, meaning that if you don’t plan to pay off your credit card bills and balance in full at the end of each month, you’re going to be paying huge interest costs and fees that frankly are un-necessary. You’re basically flushing money that you’ve earnt down the toilet, most likely just to allow you to buy a non-essential item that you probably could have waited a few more months for.

Whilst credit cards definitely do have plenty of benefits, those benefits immediately lose all of their value the minute you stop paying off your balance in full, and start paying the credit card company in interest instead – which is exactly what they’re hoping that you do. So follow my straightforward rule when you get a credit card – set up a direct debit to pay off the balance in full at the end of each month, and then if you can’t afford to buy something with your credit card In cash when you make the purchase, don’t buy it until you can. Weighing yourself down with credit card debt and pay day loans creates a nightmare that’s very difficult to escape – a nightmare that will put you into a never ending cycle of being poorer than you should be.

4. Paying Too Much In Taxes

If you live in the UK then there’s 2 things in life that you can be certain will happen to: death, and paying a sh1t load of taxes.

Without a doubt, taxes are going to be the single biggest expense that you incur in your life, and whilst from a moral perspective it is important to contribute to the tax pool, it’s equally important that you use whatever legal means are available – of which there are many – to avoid paying more than your fair share in taxes, which, over the long term is going to put you in a far worse financial position than those who act smart and don’t.

Whilst finding ways to legally reduce the amount of tax that you pay might sound like an activity that only the wealthy can participate in with the help of their tax advisors – it’s actually not, in fact, there are some actions that you can take right away that will provide you with immediate tax savings that you can use to improve your financial position and security.

For example, if you do already have some savings to hand, rather than let them sit in your savings account earning minimal interest and losing value by the day thanks to our high levels of inflation, you can transfer them to an Individual Savings Account – or an ISA – which is a special type of account that typically offers higher levels of interest and the ability to invest in companies and receive dividends and capital growth – with any gains that you make in that account being completely sheltered from tax, no matter how much profit you make. So if you don’t have an ISA already and you’re just letting your savings dwindle away in an ordinary account – get one asap.

5. Not Investing Money / Doing anything with Savings

If you’ve gotten to the point of being able to consistently save some of your income in order to safeguard your financial security, then don’t start congratulating yourself just yet, because this next bad money habit might just apply to you… and that’s leaving all of your savings in a low paying interest account, rather than investing and getting your money to work for you.

Regardless of your background and intellect, if you’ve got spare capital that you’re not going to need in the next few years, it’s important to consider investing it, so that you can experience high levels of growth, and at the very least ensure that your retirement savings don’t dwindle away thanks to the power of inflation. Whilst investing might sounds like a scary topic that only the super intelligent might be able to understand, it’s not and these days you can get started with just £100 and half an hour of your time after watching some tutorials.

Over the course of the past 5 years, I’ve consistently saved and then invested a portion of my income into the stock markets, and although doing that alone hasn’t turned me into a multi-millionaire, what it has done is grown my savings to a far higher amount and given me far more financial flexibility than if I just left them in a bank account. My only regret with investing is that I didn’t get started sooner – so don’t make the same mistake that I did, and if you do have savings that are sat in a low paying account, don’t be afraid to invest a portion of them in order to grow your wealth and improve your financial position.

Here’s my blog post on how to invest your first £100 if you want a step-by-step investing guide for beginners.

6. Getting A Side Hustle

In this day and age, it’s becoming more and more important to give yourself an additional layer of financial protection by generating more income from a side hustle. Whilst you might feel secure with your job and the earnings that it provides, there’s never going to be a guarantee that your employer doesn’t need to make cutbacks and fire you, or that they’ll give you that payrise that you think you deserve. More importantly though, unless you have a job that’s in a well paying industry – of which those are becoming few an far between, just sticking with a single income stream in the context of the current cost of living crisis, that’s only going to result in you becoming poorer over time after adjusting for inflation. Getting a side hustle is something that can not only improve your financial position, but give you the confidence and skillset to build numerous income streams, supercharging your earnings and putting you the path to achieve financial freedom again.

5 years ago I took the decision to start a side hustle, by learning how to sell products on Amazon – and since then, I’ve created a 7-figure business, I’ve learnt how to network, how to import, and ultimately how to increase my wealth far beyond what I ever thought was possible. So my final bad habit for you to avoid is not starting a side hustle. Watch my Amazon webinar if that sounds of interest, or browse YouTube for ideas – whatever you do for idea generation, it doesn’t matter, just get on the path to making a side hustle if you want to give yourselves chance of financial freedom.

Conclusion

Hopefully, this summary of the most common bad money habits that I see helps you to fix yours if any apply to you. It’s important to note that putting yourself on a path towards financial freedom isn’t going to be a case of fixing one single bad habit, but fixing them all whilst continuously looking for as many ways as possible to improve personal finances and grow your wealth and financial position.

If you want to learn how you can create an Amazon FBA business yourself, then check out my free training where I’ll teach you everything you need to launch your first product on Amazon and scale to $5,000+ in monthly profit.

Or if you’re ready to begin your journey and want to start with the best chances of success, apply to become a member of HonestFBA’s training programme where you’ll receive guidance & support from our team of 7-figure Amazon FBA seller experts whenever you need it.